How to Get a Fair Cash Offer on Your Home

When you’re facing divorce, foreclosure, or a financial crisis, selling your home fast can feel like your only way out. But knowing how to get a fair cash offer is what separates sellers who protect their equity from those who give it away. Cash buyers are not all the same. Some are legitimate investors ready to close in days. Others are wholesalers who will tie up your property and walk away. This guide gives you the tools to tell the difference, verify every offer, and negotiate terms that actually work in your favor.

Table of Contents

- Key takeaways

- How to get a fair cash offer: know your home’s value first

- What cash buyers actually look at when making offers

- Step-by-step process to get and compare multiple cash offers

- Common mistakes to avoid when accepting cash offers

- My honest take on navigating cash offers under pressure

- How Dcbuyshouses helps you sell with confidence

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Know your home’s value first | Research your after-repair value before talking to any buyer so you have a real benchmark. |

| Benchmark fair offers at 70% ARV | Legitimate investors typically offer 60-70% of ARV; anything lower from an unverified buyer is a red flag. |

| Verify every buyer before signing | Demand proof of funds from a real financial institution and a 3% earnest money deposit. |

| Get multiple competing offers | Platforms with multiple bidders consistently produce better prices and more favorable terms. |

| Compare net proceeds, not headline numbers | Subtract all fees, repairs, and closing costs before deciding which offer is truly best. |

How to get a fair cash offer: know your home’s value first

Before you talk to a single buyer, you need a realistic number in your head. Without it, you have no way to evaluate whether an offer is fair or insulting.

After-repair value vs. current condition

Your home has two values. The first is what it’s worth right now, in its current condition. The second is the after-repair value (ARV), which is what it would sell for on the open market after all repairs and updates are complete. Cash buyers use ARV as their anchor number when calculating what to offer you.

Here’s why that matters. If your home has an ARV of $300,000 but needs $50,000 in repairs, a buyer who offers you $180,000 is actually offering you 60% of ARV. That may sound low, but it’s within the typical investor range. A buyer who offers $120,000 on that same property is trying to take advantage of you.

To find your ARV, look at recent sales of comparable homes in your neighborhood that are in good condition. These are called “comps.” You can pull them from public records, ask a local real estate agent for a comparative market analysis (CMA), or hire an appraiser for around $300 to $500. Online tools like Zillow or Redfin give you a rough starting point, but they can be off by 10% to 20% in markets with limited data. Use them to orient yourself, not to make final decisions.

Here’s what to look at when building your own value picture:

- Recent sales within the last 90 days within a half-mile radius

- Homes with similar square footage, bedroom count, and lot size

- Condition adjustments for major systems like roof, HVAC, and foundation

- Local market trends: is your area appreciating or cooling off?

Pro Tip: Ask two or three local agents for a free CMA. Most will provide one in hopes of earning your listing. You get free data, and you learn what your home is realistically worth before a single buyer walks through the door.

What cash buyers actually look at when making offers

Understanding the buyer’s math helps you negotiate from a position of knowledge rather than desperation.

How investors calculate their offers

Investors typically pay 60-70% of ARV, while owner-occupant cash buyers who plan to live in the home tend to offer 76-84% of ARV. The difference comes down to risk and profit margin. An investor needs to account for repair costs, carrying costs while the property sits during renovation, sales commissions when they resell, and their own profit. An owner-occupant just needs a home they love at a price they can afford.

Here’s a side-by-side comparison so you know what to expect:

| Buyer type | Typical offer range | Closing timeline | Best for |

|---|---|---|---|

| Real estate investor | 60-70% of ARV | 7-14 days | Heavily distressed properties |

| Owner-occupant cash buyer | 76-84% of ARV | 14-30 days | Move-in ready or light repairs |

| iBuyer platform | 70-80% of ARV | 14-21 days | Mid-range condition homes |

| Wholesaler | 50-65% of ARV | Often delays or falls through | Avoid unless you understand the risk |

Cash offers allow faster closings without appraisal or financing contingencies, which is a real advantage when you need certainty. That speed and certainty is worth something, and it justifies accepting a price slightly below what you’d get from a financed buyer who might back out three weeks before closing.

Watch for these buyer behaviors that signal a serious, legitimate offer:

- Proof of funds provided within 24 hours of request

- A 3% non-contingent earnest money deposit held by a neutral title company

- A clear closing timeline of 7 to 14 days

- No request for upfront fees from you

Pro Tip: A legitimate cash buyer expects you to do your homework. If a buyer gets uncomfortable when you ask for proof of funds or want your attorney to review the contract, that discomfort is your answer. Walk away.

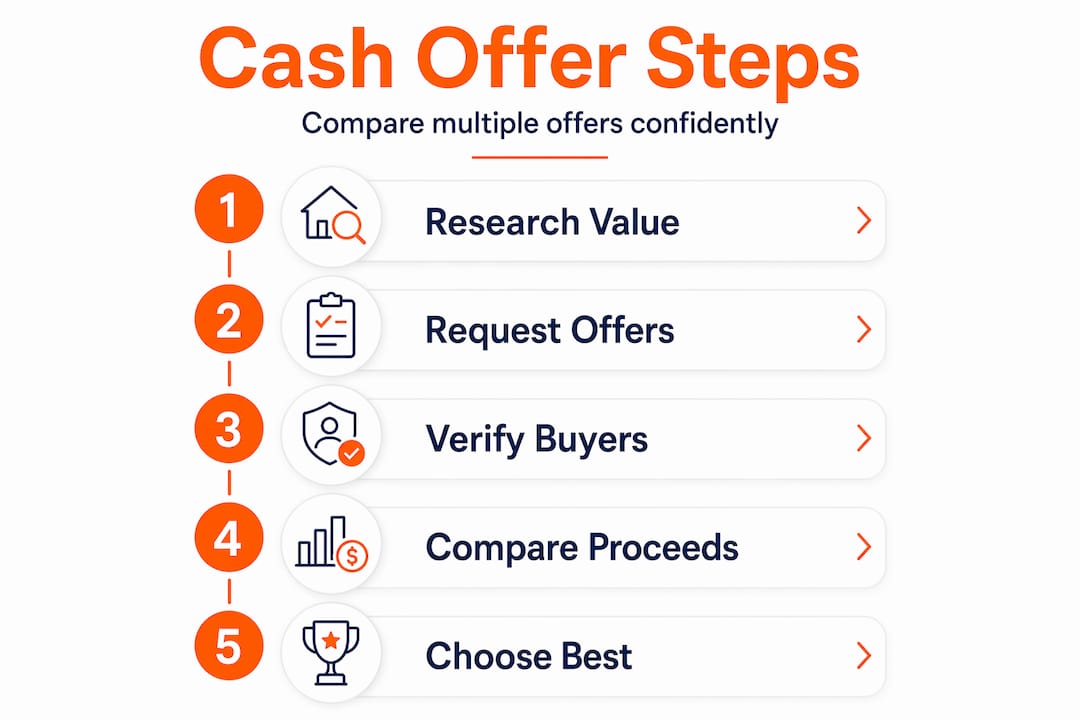

Step-by-step process to get and compare multiple cash offers

This is where most sellers leave money on the table. They take the first offer they receive because they’re under pressure. Getting multiple offers is the single most effective way to maximize your cash offer.

Step 1: Create broad exposure to cash buyers

Start with these sources:

- Direct cash buyers in your local market (search “[your city] we buy houses”)

- iBuyer platforms that generate instant online offers

- Real estate investor networks and local real estate investment association (REIA) meetings

- Competitive offer platforms that submit your property to multiple buyers simultaneously

Platforms that generate multiple competing offers consistently produce better pricing and more transparent terms versus going to a single investor. Competition works in your favor.

Step 2: Verify every buyer before you engage

Do not waste time negotiating with buyers you haven’t vetted. Ask for:

- A proof of funds letter from a legitimate bank or closing entity. Screenshots and blurred bank statements do not count.

- Their track record: How many homes have they purchased in the last 12 months? Can they provide references from past sellers?

- Their earnest money policy: A $1,000 deposit signals low commitment. A 3% non-contingent deposit held by a title company signals a serious buyer.

Step 3: Review contract terms carefully

The headline price is not the whole story. Before you sign anything, check for:

- “And/or assigns” language in the buyer’s name field. This allows contract assignment to another investor without your consent. Remove it.

- Unlimited or vague inspection contingencies that give buyers an easy exit

- Closing timelines longer than 30 days, which often signal a wholesaling deal

- Any clause requiring you to pay fees before closing

Step 4: Build a net sheet for each offer

A higher offer number does not always mean more money in your pocket. Build a simple net sheet for each offer:

| Item | Example offer A | Example offer B |

|---|---|---|

| Offer price | $210,000 | $195,000 |

| Seller-paid closing costs | ($6,000) | ($0) |

| Repair concessions | ($10,000) | ($0) |

| Your net proceeds | $194,000 | $195,000 |

Net proceeds comparison is what actually matters. Subtract all commissions, repair costs, holding costs, and fees from each offer before making your decision. Offer B above is actually better despite looking lower on paper.

Common mistakes to avoid when accepting cash offers

Sellers under financial pressure are exactly who bad actors target. Knowing these pitfalls protects you.

- Skipping buyer verification. Never accept an offer from someone who won’t provide proof of funds within 24 hours. Delays and excuses are red flags, not explanations.

- Ignoring contract language. The “and/or assigns” clause is the most common contract trap. It lets a wholesaler flip your contract to another investor, often causing your sale to fall apart at the last minute.

- Caving to pressure tactics. Scam buyers demand immediate signatures, refuse to allow attorney review, or charge upfront fees. Legitimate buyers give you time to review.

- Accepting the first offer out of fear. Even in urgent situations, taking 48 to 72 hours to get two or three competing offers can mean tens of thousands of dollars more in your pocket.

- Ignoring your ARV benchmark. If you don’t know your home’s after-repair value, you have no way to know whether an offer is reasonable. Do the math before you negotiate.

“The most expensive mistake a distressed seller can make is signing a contract without understanding what they’re actually agreeing to. A fair offer is one you can verify, not just one that sounds good over the phone.”

If you’re also facing foreclosure, learning your options to avoid foreclosure before you accept any offer can protect your credit and give you more negotiating leverage than you realize.

My honest take on navigating cash offers under pressure

I’ve worked with sellers going through divorce, probate, fire damage, and pre-foreclosure. And I’ll tell you what I’ve seen repeatedly: the sellers who get the best outcomes are not the ones who got lucky. They’re the ones who slowed down just enough to get informed before they signed anything.

Here’s what I’ve learned that most articles won’t tell you. Waiting for a retail buyer is not always the wrong choice, but it’s also not always an option. When your mortgage is 90 days past due or your divorce attorney needs the asset liquidated, time is not on your side. The goal is not to get the highest possible price. The goal is to get the fairest possible price given your actual timeline and situation.

I’ve seen sellers walk away from legitimate offers at 68% of ARV because they held out for something better, only to end up accepting 58% three months later after carrying costs ate into their equity. I’ve also seen sellers accept the very first offer they received from an unverified buyer, only to have the deal fall apart two weeks before closing because it was a wholesaling assignment that never had real funding behind it.

What actually works is creating competition. When three or four buyers know they’re competing for the same property, offers go up and terms get better. I’ve watched that dynamic add $15,000 to $30,000 to a seller’s net proceeds on a single transaction. That’s not theory. That’s what happens when you treat your home like an asset worth protecting, even when you’re under pressure.

Know your ARV. Verify every buyer. Get multiple offers. And if something feels off about a contract or a buyer, trust that instinct. It’s usually right.

— Danny

How Dcbuyshouses helps you sell with confidence

When you’re dealing with foreclosure, divorce, or any situation that demands a fast sale, you deserve more than a lowball offer from an unverified buyer.

Dcbuyshouses connects homeowners with verified cash buyers who compete for your property, which means better prices and real transparency from day one. Every buyer in the network provides proof of funds and a serious earnest money deposit. You get a clear, no-obligation offer with a closing timeline that fits your situation, not theirs. See exactly how the process works and what you can expect at every step. If you’re ready to get a real number on your home, start with a free property evaluation at Dcbuyshouses and find out what your home is actually worth to a verified cash buyer today.

FAQ

What is a fair cash offer on a house?

A fair cash offer is generally at least 70% of your home’s ARV from a verified buyer who provides proof of funds and a non-contingent earnest money deposit. Anything significantly below that threshold from an unverified buyer warrants serious scrutiny.

How fast should a legitimate cash buyer close?

A serious cash buyer should close within 7 to 14 days. Offers requiring 30 or more days to close often indicate a wholesaling deal rather than a direct purchase, which carries a higher risk of the deal falling apart.

How do I verify a cash buyer is legitimate?

Request a proof of funds letter from a recognized financial institution or title company within 24 hours of your request. Vague screenshots or blurred statements do not qualify as valid proof of funds and should be treated as a red flag.

Should I accept the first cash offer I receive?

No. Getting at least two to three competing offers is one of the best cash offer strategies available to you. Competitive bidding consistently produces better prices and terms than going with a single buyer, even when you’re under time pressure.

What contract terms should I watch out for?

The most dangerous clause is “and/or assigns,” which allows a buyer to transfer your contract to another investor without your approval. Remove this language before signing, and watch for vague inspection contingencies or any requirement to pay fees before closing.